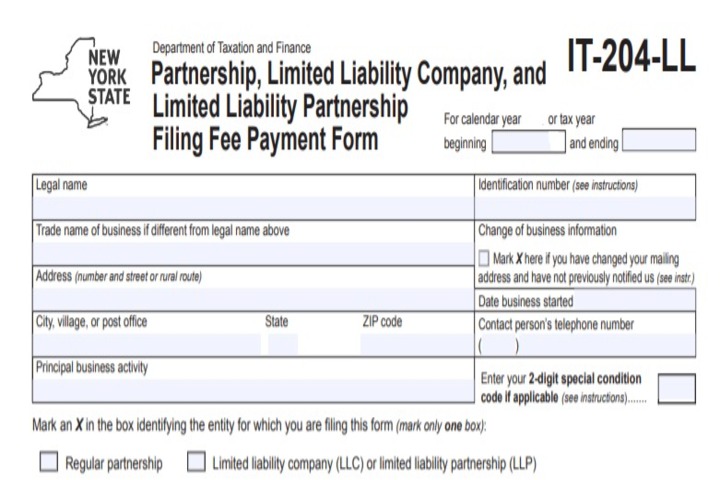

Instructions For Form IT-204-LL

Instructions for Form IT-204-LL Partnership, Limited Liability Company, and Limited Liability Partnership Filing Fee Payment Form.

Who Must File:

-

Domestic or foreign LLC (including a limited liability investment company (LLIC) or a limited liability trust company (LLTC)), or limited liability partnership (LLP) which is required to file a New York State partnership return and which has income, gain, loss, or deduction from New York State sources; and

-

Limited liability company that is a disregarded entity for federal income tax purposes and having income, loss, or deduction from New York State sources, and

-

Regular partnership (those that are not an LLC or LLP) that is required to file a New York partnership return that has income, gain, loss, or deduction from New York State sources, and had New York source gross income for the preceding tax year of at least $1 million.

Who Must not File:

-

A partnership, LLC, or LLP with no income, gain, loss, or deduction from New York sources who is filing a partnership return solely because it has a New York resident partner; or

-

A partnership, LLC, or LLP with no income, gain, loss, or deduction from New York sources regardless of whether or not it is formed under the laws of New York State or is dormant; or

-

An LLC or LLP that has elected to be treated as a corporation for federal income tax purposes.

How to compute filing Fee?

The amount of the filing fee will be based on the New York source gross income for the tax year immediately preceding the tax year for which the fee is due. If the LLC or LLP did not have any New York source gross income for the preceding tax year, the filing fee is $25.

How to compute New York source gross income?

It is the sum of the partners’ or members’ shares of federal gross income from the partnership, LLP, or LLC, derived from or connected with New York State sources without any allowance or deduction for cost of goods sold, determined in accordance with the provisions of section 631 of the New York State Tax Law as if those provisions and any related provisions expressly referred to a computation of federal gross income from New York sources.

When to file:

Form IT-204-LL must be filed on or before the 15th day of the third month following the close of your tax year. Full remittance of any filing fee due should be submitted with this form.

Extension of time to file:

There is no extension of time to file Form IT-204-LL or pay the annual fee.

Amended Form IT-204-LL:

Amended Form IT-204-LL must be filed to correct an error on your previously filed Form IT-204-LL or to report changes.

NYS filing fee:

| If the New York source gross income on line 4 is more than: | but not more than: | LLC/LLP enter on line 5: |

|---|---|---|

| $ 0 | $ 100,000 | 25 |

| 100,000 | 250,000 | 50 |

| 250,000 | 500,000 | 175 |

| 500,000 | 1,000,000 | 500 |

| 1,000,000 | 5,000,000 | 1500 |

| 5,000,000 | 25,000,000 | 3000 |

| 25,000,000 | 4500 |

Do you need a more Instructions For Form IT-204-LL or plan to hire a tax advisor in new york? Connect with our team today by filling the below form or you call us on (+1) 718-426-4661 or email us at baggarwal@aggarwalcpa.com